Over the last several years, women’s financial inclusion has been growing rapidly, particularly in low- to medium-income countries. The World Bank Group’s Global Findex 2025 Report shows a significant increase in the number of women with access to financial accounts. In 2024, nearly three-quarters (73%) of women living in these lower- and middle-income countries will own a financial account, compared with only 66% (a 7 percentage point increase) in 2021. This increase is strong evidence that women are being given more access to financial services and are now being integrated into the formal financial system.

Financial accounts provide women with access to a variety of important financial products and services, including savings, borrowing, and payments. Recent findings also indicate that more women are now actively using their accounts for financial transactions. For example, 36% of women in LMI countries had formally saved money in 2024, compared with 22% in 2021. Additionally, the percentage of digital payment usage increased from 50% to 58% between the years 2021 and 2024. Likewise, digital merchant (payment) transactions were up from 32% to 38 minutes during the same period. These results suggest that women are increasingly embracing digital financial instruments, as well as integrating them into their day-to-day economic activities. Although many strides have been made in improving women’s financial inclusion, large disparities still exist worldwide. Over 700 million women globally are without a financial account of any kind and therefore cannot fully take advantage of all the services provided by the financial industry that would help them build wealth, save money, and invest. As such, increased access to financial accounts continues to be one of the greatest challenges facing policymakers and financial service providers.

Barriers exist for women when it comes to financial accounts and their use. One such barrier is the perception that women do not have enough funds for a minimum balance requirement. High fees charged by banks can also discourage women from opening accounts. In some areas, women are discouraged from opening accounts and instead use accounts owned by other family members; this is due in part to the high cost of financial services available in those areas. Accessing financial establishments remains a challenge throughout much of developing nations. For women who live in rural or isolated locales, distance may prevent anyone from reaching their financial institution or agent to access services; therefore, the lack of access limits account ownership for many women and reduces their ability to participate formally in financial activities. Nevertheless, the development of digital technologies is significantly changing the way people can access financial institutions. Both mobile phones and digital accounts are helping to overcome impediments to distance and expenses.

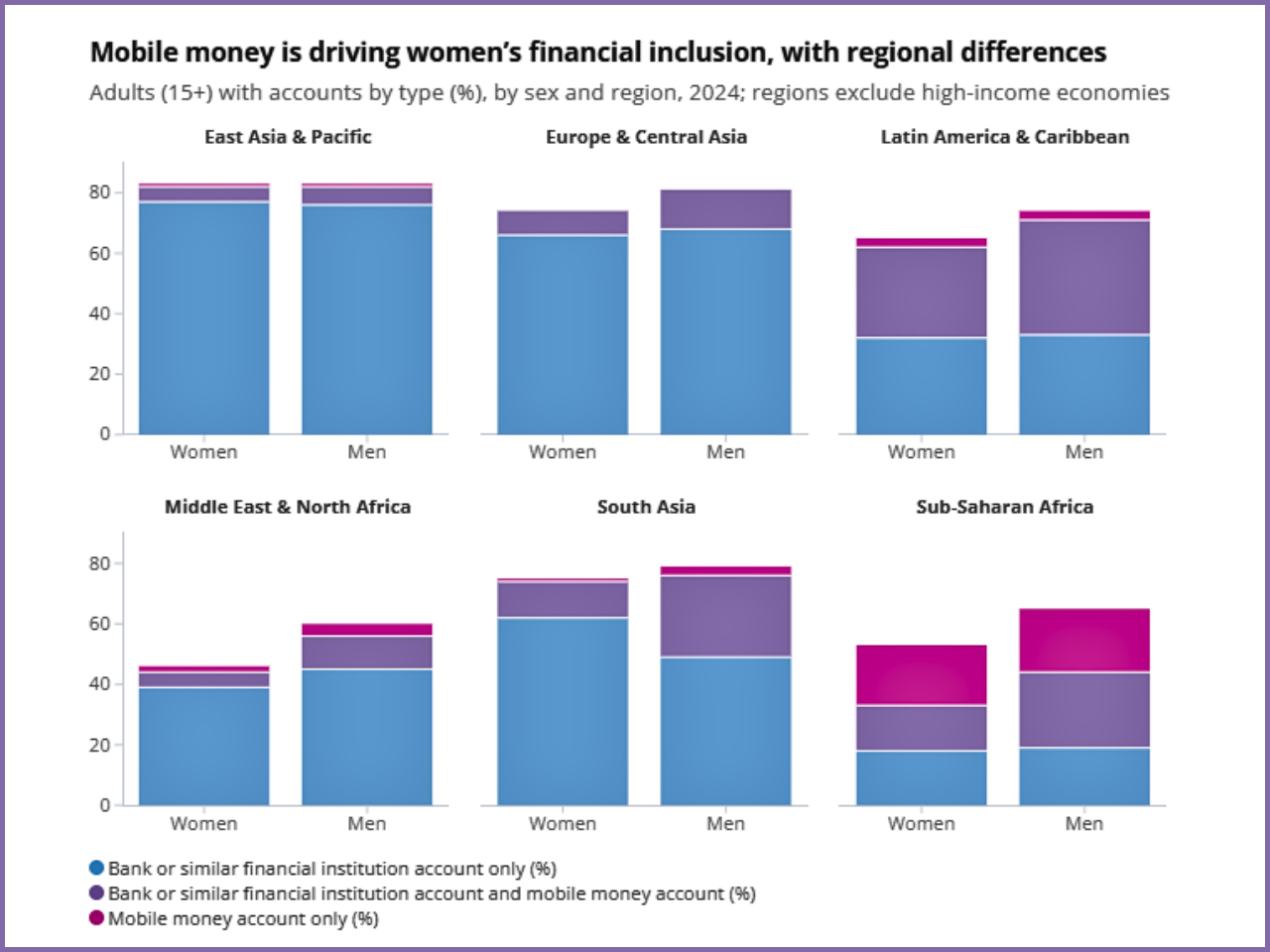

Ali Mitchell, Head of Product Management at Western Union, states that digital accounts allow individuals to conduct their financial activities at any time or in any location, which makes it far easier to use and access the financial system. As such, currently more than half (50%) of women who have an account in low- and middle-income countries have a digitally enabled account that can be used via a mobile phone or debit/credit card. Women’s mobile phone ownership greatly increases access to digital financial services. In developing nations, approximately 80% of women own mobile phones, providing women with access to digital payment systems and mobile banking. Mobile money services allow individuals in Sub-Saharan Africa and Bangladesh to conduct transactions using a basic device at a much lower cost than traditional banking methods. Mobile money accounts provide women access to financial resources, thereby alleviating the gender disparity between men and women when accessing financial resources. While less than half of women have access to formal financial services through mobile money accounts, the ability to access these services is an equal opportunity between men and women. However, a significant percentage of women do not own devices that allow them access to digital payment options and therefore have limited access to financial services; digital payments such as wages and government remittances motivate women to open financial accounts and obtain connections to formal financial institutions. There are a large number of unbanked women (10%) in low- and middle-income countries receiving wages or government payments but who have not yet opened an account to receive the payments electronically.

Encouraging digital payments has the potential to bring millions of women into the financial system. However, just having financial accounts is not enough. Real financial inclusion means that women use financial services. Many women who have accounts are still having trouble using their accounts. Research shows that women are less likely than men to save or access loans from formal financial institutions or use digital payment methods regularly, which suggests that financial services may not always be created to meet women’s needs. Women have difficulty accessing credit, with only 9% of women borrowing money to start or run a business, and only 50% of the women that do so will receive loans from formal financial institutions. Limited access to formal credit decreases the opportunity for women to grow their businesses and increase their economic independence. The World Bank Group has set a goal of financing 80 million women and women-owned businesses by 2030 to address the lack of access to financing.

Women in low- and middle-income countries also have low levels of financial resilience. Women in these countries do not feel as confident as men regarding the access to emergency funds for unexpected financial emergencies that may occur (i.e., job loss or property damage). Many women use the informal assistance of family and friends. Having an active account and utilizing it can assist women with developing savings and preparing for any economic disasters that may arise. Women’s financial inclusion is on the rise due to more accounts being obtainable and a rise in the availability of digital finance; however, there are many women who remain excluded due primarily to high fees, lack of knowledge about finance, or inability to access internet or phone service. To achieve universal financial inclusion will require cooperation between all three parties: the government, financial institutions, and the world community that provides resources.